Aadhar Housing Finance Ltd has quietly emerged as a standout in India’s competitive housing finance market. While the spotlight has been on Bajaj Housing Finance’s upcoming public issue, Aadhar’s shares have surged 33% since its May debut.

It’s likely that Blackstone, which still holds a 76% stake in Aadhar, is eyeing even larger gains, driven by the attractive dynamics of the affordable home loan segment, with loans under ₹25 lakh. Having largely recouped its ₹2,200 crore acquisition cost, paid in FY20, through an offer for sale, Blackstone has already multiplied its investment nearly sevenfold.

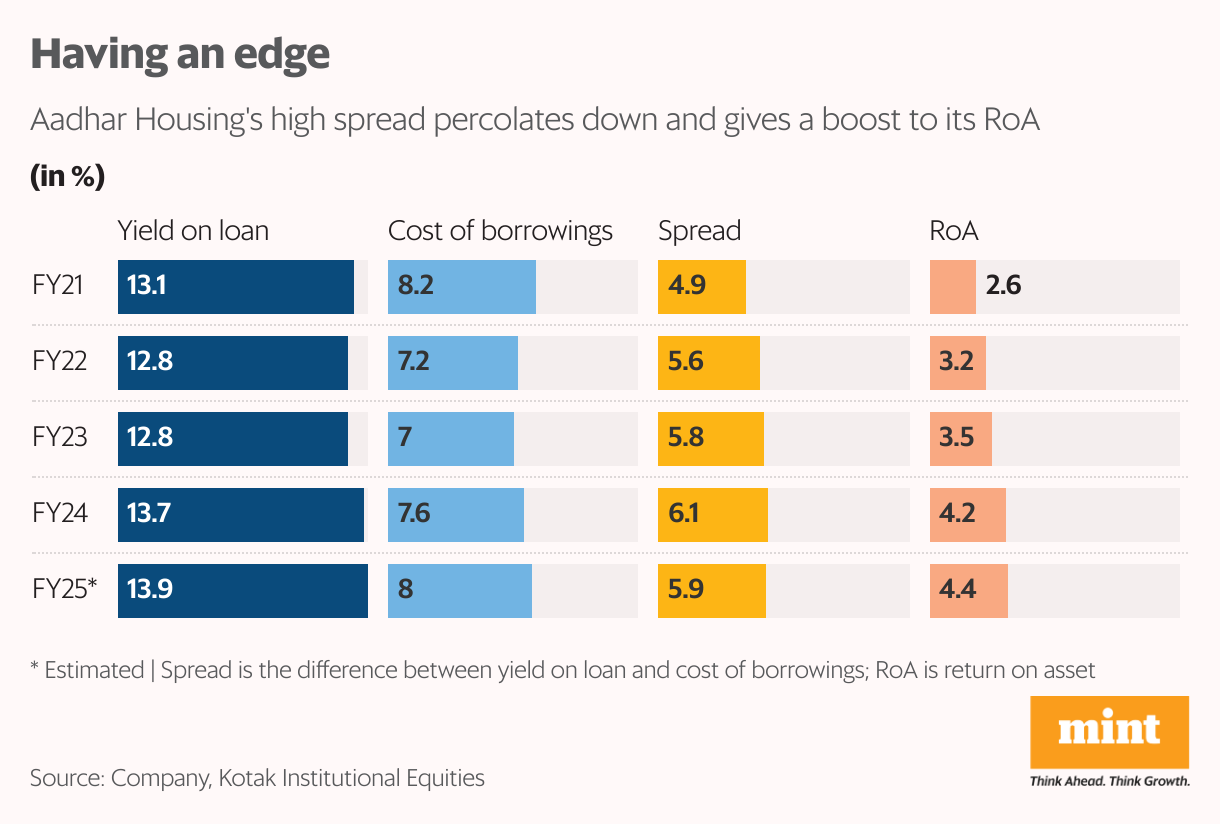

Niche market and attractive margins

An appealing feature of affordable housing finance is the healthy spreads. For FY24, the industry’s median interest rates charged stood at 13.2% and cost of borrowings at 8.4%, resulting in a spread of 4.8%. Aadhar stands out, given its higher spread of 6.1%. Consequently, its RoA (return on asset) is 4% plus.

Notably, other housing non-banking financial companies focused on prime category, where the loan value is typically more than ₹50 lakh, such as Bajaj Housing Finance have an RoA of 2.5% for FY24 mainly because they charge relatively lower interest rates to borrowers.

Analysts from Kotak Institutional Equities expect Aadhar to grow its assets under management (AUM) by 21% over FY24-27. In comparison, Crisil Market Intelligence & Analytics expects the affordable housing finance industry to pick up steam gradually to touch ₹14.4 trillion by FY27 with a CAGR of 10%, much higher than about 6% CAGR seen during FY21-24.

According to Crisil, reasons for the higher growth include increased budgetary support and incentives from central and state government; and high affordable loan demand from tier 3 and tier 4 cities in the post covid world.

Read this | LIC Housing Fin to bank on affordable housing loans for credit growth, margins

The key question then is whether Aadhar can continue to outperform the industry growth rate.Its track record suggests it can. Between FY21 and FY24, the company achieved a 16% CAGR in AUM, and it has provided guidance for 20-22% growth in FY25.

It helps that Aadhar has a geographically diversified AUM mix with no single state contributing more than 15%. Loans to salaried account for 57% of the total, with the remainder going to self-employed borrowers. While the overall credit cost for FY24 was at 0.2%, in line with the industry average, Kotak has flagged potential risks from the non-salaried segment. This stems from Aadhar’s limited experience with self-employed borrowers, who tend to be more volatile compared to salaried customers, typically more resilient to economic cycles.

Also read | Mint Explainer: How affordable housing in urban areas got a Budget boost

Against this backdrop, the stock’s reasonable valuation—currently at a price-to-book ratio of 2.4x based on FY26 book value projections by ICICI Securities and Kotak—offers some comfort.

link

More Stories

Why Operational Excellence Has Become the Defining Advantage in Private Equity

We built this city on development charges…

Making Homes Make Cents: How Affordable Housing is Financed