Sustainability is expected to soon become a cornerstone of the

regulatory environment. The non-financial aspects of an investment

will be increasingly emphasised during the decision-making process.

Greenwashing will no longer be enough; environmental and social

aspects will truly matter as investors and society turn their

attention to them. This will challenge how the lending sector

operates and it must prepare for the transition as soon as

possible. This overview aims to shed light on the government and

regulatory programmes in the CEE-SEE region, to smooth the

transition by making the investments more attractive and

profitable.

Please click here to view interactive map

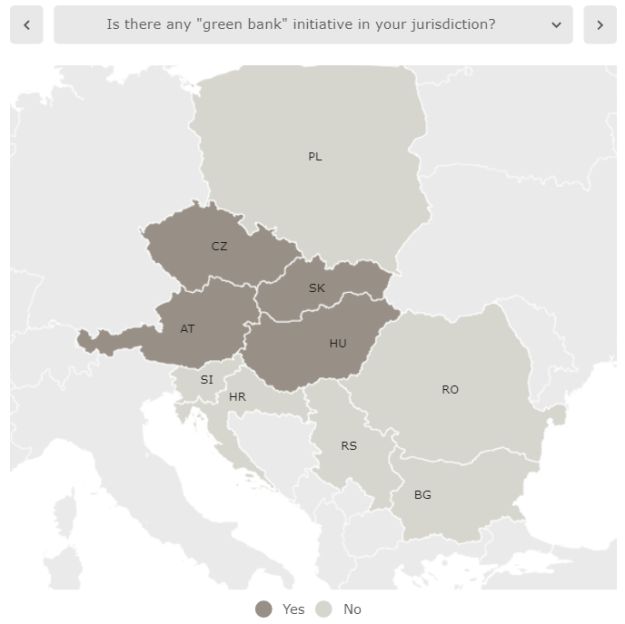

Is there any “green bank” initiative in your

jurisdiction?

Austria

Yes.

Green Finance Alliance: The Austrian Federal

Ministry for Climate Action, Environment, Energy, Mobility,

Innovation and Technology launched the Green Finance Alliance, an

initiative aimed at establishing a sustainable financial market in

Austria. Its members are financial institutions who aim to achieve

climate neutrality by 2050.

Bulgaria

No.

There is no local initiative by the Bulgarian regulator of the

banking sector – the Bulgarian National Bank. Nevertheless, the

Bulgarian Development Bank, whose sole owner is the Bulgarian

state, aims to help small and medium-sized enterprises in this

aspect, as the Strategy of the Bulgarian Development Bank for the

2021-2023 period envisages 20 % of the new loans to be green

(compliant with ESG) -

https://bbr.bg/en/news-bbr/bdb-will-help-small-companies-green-transition/

Croatia

No (at this point).

There is no “green bank” initiative by the Croatian

National Bank (the CNB) yet. However, at the start of November

2021, the CNB made a public “Climate Pledge” in which

(given its mandate, instruments and resources) it declared its

determination to strengthen its catalytic role in fostering climate

transition in Croatia. In that respect, the goals of the CNB

include: (i) building and enhancing its staff’s skills and

knowledge on the impact of climate change on the CNB’s main

goals; (ii) developing and subsequently implementing its own

climate strategy and allocating adequate resources to address

climate-related and environmental risks in different policy areas,

especially in the area of financial stability, supervision,

research, monetary operations and foreign reserves management;

(iii) incorporating climate-related and environmental risks into

supervisory expectations in line with the ECB’s Guide on

climate-related and environmental risks; (iv) engaging in regular

open dialogue with credit institutions in order to encourage them

to incorporate climate-related and environmental risks into their

risk management frameworks and decision-making processes; (v)

supporting the establishment of a workstream within the Vienna

Initiative charged with exploring how it can assist credit

institutions in adapting to climate transition and transforming

economies in line with European climate goals; and (vi) formulating

an action plan by the end of 2022, aimed at reducing its own carbon

footprint in line with the Paris Agreement objective of limiting

global warming to 1.5 degrees Celsius. This last action plan was

not yet published, presumably because Croatia is entering the

eurozone in 2023 and the CNB is converging its policies with the

ECB.

Czech Republic

Yes.

In the first quarter of 2021, 16 members of the Czech Bank

Association signed a Sustainable Finance Memorandum. The Memorandum

binds the members to minimise the impacts of their operations on

the environment, to continue to digitise and transition to

paperless procedures, to cooperate with public authorities, to exit

loan portfolios associated with production that is excessively

harmful to the environment or human health or to offer services and

green finance products (obligations, mortgages or loans)

contributing to sustainability.

Hungary

Yes.

In April 2021, the Hungarian National Bank issued a Green

Recommendation to encourage Hungarian credit institutions to modify

their operations towards sustainability, including strategy making,

corporate governance, risk management, etc.

Poland

No.

The Polish legislation does not define a “green bank”,

but there are numerous governmental projects in which the presence

of a bank is important. An example of such a project is the

“Clean Air Programme” created by the Ministry of Climate

and Environment. Banks were invited to apply to participate in the

programme, which resulted in the launch of a new banking pathway

entitled “Green Bank”. “Clean Air Credit”. The

project concerns subsidies for the replacement of heat sources up

to a certain amount for owners of single-family houses and

dwellings in municipalities that fall under the so-called anti-smog

law.

Romania

No.

Apart from the EU initiatives, no specific Romanian green bank

initiatives exist.

Serbia

No.

So far, there have been no “green bank” initiatives in

Serbia. However, in 2021, the National Bank of Serbia (NBS) became

a member of the global Network of Central Banks and Supervisors for

Greening the Financial System (NGFS). The NBS has declared its

support for scaling up green finance in Serbia and for

transitioning toward a sustainable economy. Meanwhile, major

commercial banks in Serbia have sustainability and green financing

high on their agenda, evidenced by ever-growing volumes of green

and sustainability-linked lending in Serbia.

Slovakia

Yes.

In October 2021, six members of the Slovak Bank Association

signed a Sustainable Finance Memorandum that binds members to

actively cooperate with the competent authorities to implement

standards and procedures for achieving energy efficiency targets

for buildings within the meaning of the European Green Deal, to

apply sustainability principles in their business activities and

relationships, to initiate the creation of a sector standard for

ESG certification of corporate clients, and to offer services and

green financial products, investment products or loans contributing

to sustainability so that sustainable finance is accessible.

Slovenia

No.

Apart from the EU initiatives, no specific Slovenian green bank

initiatives exist.

Is there a regulatory, financial or legal incentive to

financing green projects by lending?

Austria

Yes.

Austrian Green Investment Pioneers Programme:

The Austrian Federal Ministry for Climate Action, Environment,

Energy, Mobility, Innovation and Technology implemented the

Austrian Green Investment Pioneers Programme as a part of the

klimaaktiv climate protection initiative. Participants

gain support when looking for financing for their climate-relevant

business ideas in the area of renewable energy, energy efficiency,

mobility and agriculture/bioeconomy. Lenders are encouraged to

participate as financiers in the network.

Bulgaria

No.

There is no local legal or regulatory incentive related to

financing green projects, e.g. related to interest premiums or

capital reliefs

Croatia

No.

There are no regulatory, financial or legal incentives

specifically to finance green projects by lending. However, credit

institutions in Croatia have broadened potential credit lines to

green projects, raising awareness of the Corporate Sustainability

Reporting Directive and obligations provided therein.

Czech Republic

No.

There are no regulations or incentives issued by the Czech

legislator or the Czech National Bank. Some banks provide EKO loans

and help with submission of applications to the New Green Savings

subsidy programme. However, those banks are not in any way

officially connected to the programme.

Hungary

Yes.

Hungarian banks can apply a significantly reduced capital

requirement for loans financing the purchase and construction of

energy-efficient properties. It also covers solar power plants,

sustainable agriculture, energy efficiency and electromobility. The

capital discount is 5 % or 7 % of each eligible gross exposure,

which reduces the Pillar II capital requirements of the

participating institution.

The Green Home Programme was launched during the summer of 2021

by the Hungarian National Bank. Under this programme, the MNB

provides refinancing to banks financing the construction and

purchase of green homes.

Poland

Yes.

As a rule, the state does not offer any legal or financial

benefits to the banks. The government, however, tries to direct and

motivate society to pay more and more attention to environmental

issues. For several years now, the Institute for Responsible

Finance and the UN Global Compact Network Poland, together with the

Ministry of Finance and the Ministry of Funds and Regional Policy,

have been creating a project called “Green Finance”, a

report that outlines the goals and challenges of green finance. Its

main objective is to outline the situation of sustainable

development in Polish society and in the economy, urging banks and

defining the goals they should meet. It is not only a statement by

government bodies, but also representatives of the biggest Polish

banks (e.g. PKO Bank Polski and mBank) have included their views on

the situation of “green finance”. Although the state does

not offer specific benefits to the banks, the banks themselves are

accommodating in terms of lowering interest rates on green loans

(e.g. loans for building a house with documented low energy

consumption) or offering a better margin. This is an increasingly

common practice in the banking market and more and more banks are

opting for such measures (e.g. Credit Agricole or PKO BP).

Romania

Yes and No.

While there are no specific financial incentives to financing

green projects by lending, there are legal/regulatory requirements

for credit institutions to develop and comply with an appropriate

credit risk strategy which should address environment, social and

governance risks, among others. Furthermore, the National Bank of

Romania (NBR) is closely monitoring the financing of green projects

on the Romanian market and in 2020 became a member of the Network

for Greening the Financial System (NGFS). The NGFS aims to improve

the analytical framework and management of climate-related and

environmental risks and to increase the role of the financial

system in financing the transition toward a sustainable economy. To

this end, the NGFS defines and promotes best practices to be

implemented within and outside membership of the NGFS and conducts

or commissions analytical work on green finance.

Finally, most Romanian credit institutions have added in their

agenda and are actively marketing ESG-related projects, while the

market has seen an increase in actually implemented/financed green

investments.

Serbia

No.

Not at present. The significant impetus is expected to come

under the ambitious Green Agenda for the Western Balkans and

various EU-supported financing instruments yet to be employed in

the region.

Currently, the multilateral development banks – such as EBRD

through its Western Balkans Sustainable Financing Facility, Green

Economy Financing Facility, and similar programmes – are supporting

commercial banks in Serbia by granting them funds to be lent and

invested in energy efficiency and renewable energy projects.

Slovakia

No.

For the time being, there are no regulations or incentives

issued by the Slovak legislator or the Slovak National Bank. Some

banks offer eco-loans and eco-mortgages and there are a couple of

projects ongoing that offer support for green projects (with a

particular focus on housing), such as the Sustainable Energy

Finance Facility in Slovakia (a sustainable energy financing

facility developed by EBRD, which is co-funded by the Ministry of

Environment of the Slovak Republic and the Ministry of Agriculture,

Food and Environment of Spain and provides a credit line of up to

EUR 100m to Slovak commercial banks) or the GreenDeal4Buildings

(Horizon 2020)

Slovenia

Yes.

For the time being, there is no regulatory or legal incentive,

but there is a financial incentive to financing green projects by

lending in Slovenia. SID Bank (a development and export bank owned

by the Republic of Slovenia) adopted the SID Green Bond Framework

in November 2018 to issue green bonds to finance and/or refinance

loans granted to projects in the fields of environment protection,

ensuring proper waste management, proper consumption of natural

resources, increasing investments in environment protection

infrastructure, encouraging the use of renewable energy sources and

encouraging efficient energy use. SID Bank funds eligible projects

by granting loans, by other types of financings (e.g. purchase of

receivables) or investing into green bonds.

Are green bonds encouraged or incentivised in your

jurisdiction? (by means of guidelines, interest premiums, capital

reliefs, etc.)?

Austria

Yes.

Vienna Stock Exchange ESG Segment: The Vienna

Stock Exchange provides a market segment devoted exclusively to

sustainable bonds: the Vienna ESG Segment. The admission principles

are based on the International Capital Market Association’s

Principles.

Bulgaria

No.

Croatia

No.

There are no such instruments with respect to any encouragements

or incentive towards green bonds. In that sense green bonds are

heavily relied upon in the market in general and to the interest of

investors. Only one green bond has been issued so far in Croatia

and it has attracted great interest from investors. So new green

bonds are to be expected in Croatia.

Czech Republic

No.

Hungary

Yes.

The MNB issued a guideline setting forth the main green bond

standards, providing issuers with a to-dos list and stipulating the

necessary documentation and reporting obligations. The Budapest

Stock Exchange also supports the development of the green bond

market by issuing ESG Reporting Guidelines presenting the content

and format standards used internationally and providing practical

help in preparing ESG reports. In addition, the MNB launched a

Green Mortgage Bond Purchase Programme for the purchase of

green-rated mortgage bonds to promote green housing lending.

Poland

Yes.

State bodies set certain targets in sustainability reports, e.g.

“Green Finance” or the “Capital Market Development

Strategy”, which devote an entire chapter to sustainable

finance. One of the most important pieces of legislation drawn up

by the Ministry of Finance is the “Green Bond Framework”,

which mirrors the Green Bond Principles by ICMA on the Polish

scene. It indicates the courses of action and the requirements to

be met by banks.

The Warsaw Stock Exchange implements the Green Bond Principles

by working with the International Finance Corporation and some law

firms. As part of the Polish Green Bond Framework programme, the

IFC offers free assistance in proper reporting, preparation of

green bond documentation or training in this area.

Romania

Yes and No.

As previously mentioned, no specific Romanian financial

incentives have been implemented. However, ESG projects are

monitored and encouraged by the market in general and by NBR in

particular, and several green bonds issuances have been implemented

in Romania during the past two years.

Serbia

Yes and No.

Green bonds are encouraged as part of a wider effort by the

Government of Serbia to deepen Serbia’s capital markets (which

remain relatively shallow to date). Save for the general

endorsement of green bonds under the Government’s “Capital

Market Development Strategy for the period 2021-2026”, no

concrete incentives have been presented yet.

A market segment that operates comparatively better is the

sovereign bond market. In August 2021, the Government of Serbia

issued the Green Bond Framework, applicable to sovereign bonds. In

September 2021, the Republic of Serbia issued its first EUR 1bln

green bond, for financing its green agenda.

Slovakia

No.

There is no incentive in terms of guidelines or interest

premiums. Some banks have already issued green bonds.

Slovenia

Yes.

Currently, Slovenian legislation does not expressly

encourage/incentivise the use of green bonds. However, SID Bank

incentivises the use of green bonds by investing into eligible

green projects which are in accordance with the SID Green Bond

Framework.

Furthermore, the Treasury of the Republic of Slovenia adopted

the Slovenian Sustainability Bond Framework (SSBF) in 2021 to fund

government investments that contribute to Slovenia’s

environmental and social goals and promote the development of the

domestic and international green bond market.

Are the eligible criteria of green projects identified by the

GBP (green bond principles) in your jurisdiction? What are the main

elements of the GBP?

Austria

N/A

Austria has no national green bond principles in the narrower

sense. Therefore, usually international guidelines are used, such

as the Green Bond Principles published by the International Capital

Market Association.

Ecolabel for Sustainable Financial Products: Already in 2004,

the Austrian Federal Ministry for Climate Action, Environment,

Energy, Mobility, Innovation and Technology created an Ecolabel for

Sustainable Financial Products (the first of its kind in Europe).

Bonds can get a certification with the Austrian Ecolabel if

projects financed via those bonds are pursuing climate projection,

adaption to climate change, sustainable use and protection of water

and marine resources, etc

Bulgaria

No.

The EU Taxonomy Regulation is directly applicable in Bulgaria,

but apart from that no other relevant domestic laws for green

projects are in place.

Croatia

No.

Czech Republic

No.

Hungary

Yes.

The first corporate green bond issuance took place in the summer

of 2020 under the MNB’s Bond Funding for Growth Scheme. This

issuance of HUF 30bln marks the kick-off for the Hungarian

corporate green bond market and has been followed by more green

bonds issuances by several other companies. The issued bonds are

all compliant with the corporate Green Bond Framework, which has

been validated by external reviewers in line with international

standards (Green Bond Principles). Therefore, the

Hungarian GBP is equivalent to the 2014 ICMA (International Capital

Market Association) Principles. Nevertheless, the Hungarian Green

Bond Framework was introduced in May 2020. The Ministry of Finance

in cooperation with the Government Debt Management Agency of

Hungary has set-up a Steering Committee. The GBP include use of

proceeds, overall investment eligibility, reporting of total

inflows, management of inflows and impact reporting.

Poland

Yes.

The Green Bond Framework drafted by the Ministry of Finance

addresses the key criteria recognised by the 2018 Green Bond

Principles. These include the use of inflows in the form of budget

allocations, grants or projects (including their evaluation and

careful selection), management of inflows and detailed reporting,

including the reporting of the total amount of allocated inflows,

the balance of remaining funds and the translation of green

projects from each qualified sector. The above criteria are also

implemented in the strategies of Polish banks, e.g. BOS Bank, which

has included ESG-related reporting (opportunity analysis and good

governance) in its strategy.

Romania

No.

No specific Romanian legislation has been enacted. In practice,

general EU-level guidelines are considered.

Serbia

Yes.

The Green Bond Framework applicable to sovereign bonds is

aligned with the Green Bond Principles (2021), published by the

International Capital Market Association focusing on the use of

proceeds, process of expenditure evaluation and selection,

management of proceeds and reporting.

Slovakia

No.

Aside from the EU Taxonomy Regulation and general EU guidelines,

Slovakia has not adopted any eligible criteria of green

projects.

Slovenia

There is no legal act prescribing the criteria for green

projects. However, the SID Green Bond Framework implements the ICMA

GBP. For each issuance of SID green bonds, the use of proceeds,

project evaluation and selection, management of proceeds, reporting

and external review will be adopted in accordance with the SID

Green Bond Framework.

Also, the SSBF Bond Framework has been prepared in accordance

with the ICMA GBP, Social Bond Principles and Sustainability Bond

Guidelines. It is based on four core components: (i) use of

proceeds; (ii) project evaluation and selection process; (iii)

management of proceeds; and (iv) reporting. It is also based on two

key recommendations: framework publication and external revie

Is there any peculiarity that you may want to share about green

financing in your jurisdiction?

Austria

Austrian Climate and Energy Fund: In 2007, the Austrian Federal

Government created the Climate and Energy Fund, which provides

financial support to researchers and enterprises who are active in

the sustainability sector.

Austria’s position on the EU Taxonomy Regulation: Austria

supports the EU Taxonomy. However, the Federal Ministry for Climate

Action, Environment, Energy, Mobility, Innovation and Technology

holds the view that technologies such as nuclear energy and fossil

gas cannot be classified as green.

Croatia

In several public occasions, the board of Hanfa (Croatian

Financial Services Supervisory Agency), who as a regulator approves

the green bond prospectus, stated that Hanfa is especially careful

about potential greenwashing and warned potential issuers of green

bonds to specifically elaborate all the green factors of the

bonds.

Poland

Although Poland was the first country in the world to

successfully issue green treasury bonds six years ago, this did not

lead to significant growth in the market. The Ministry of Finance

has made public statements about Poland’s strong potential for

green bonds, but roadblocks (in the form of limited funding for

green projects) have been encountered every step of the way. The

crucial point is that the Polish bond market is small when compared

to Western European or Scandinavian countries, meaning there is a

great deal of room for improvement. But it is also necessary to

promote any educational initiatives that will help the economy

reach the Western European level.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link

More Stories

China’s Real Estate Challenge

How a trade war and U.S. tariffs could hit Canada’s housing market – National

Housing Development Expected To Pause If Tariff Threat Turns Into Trade War