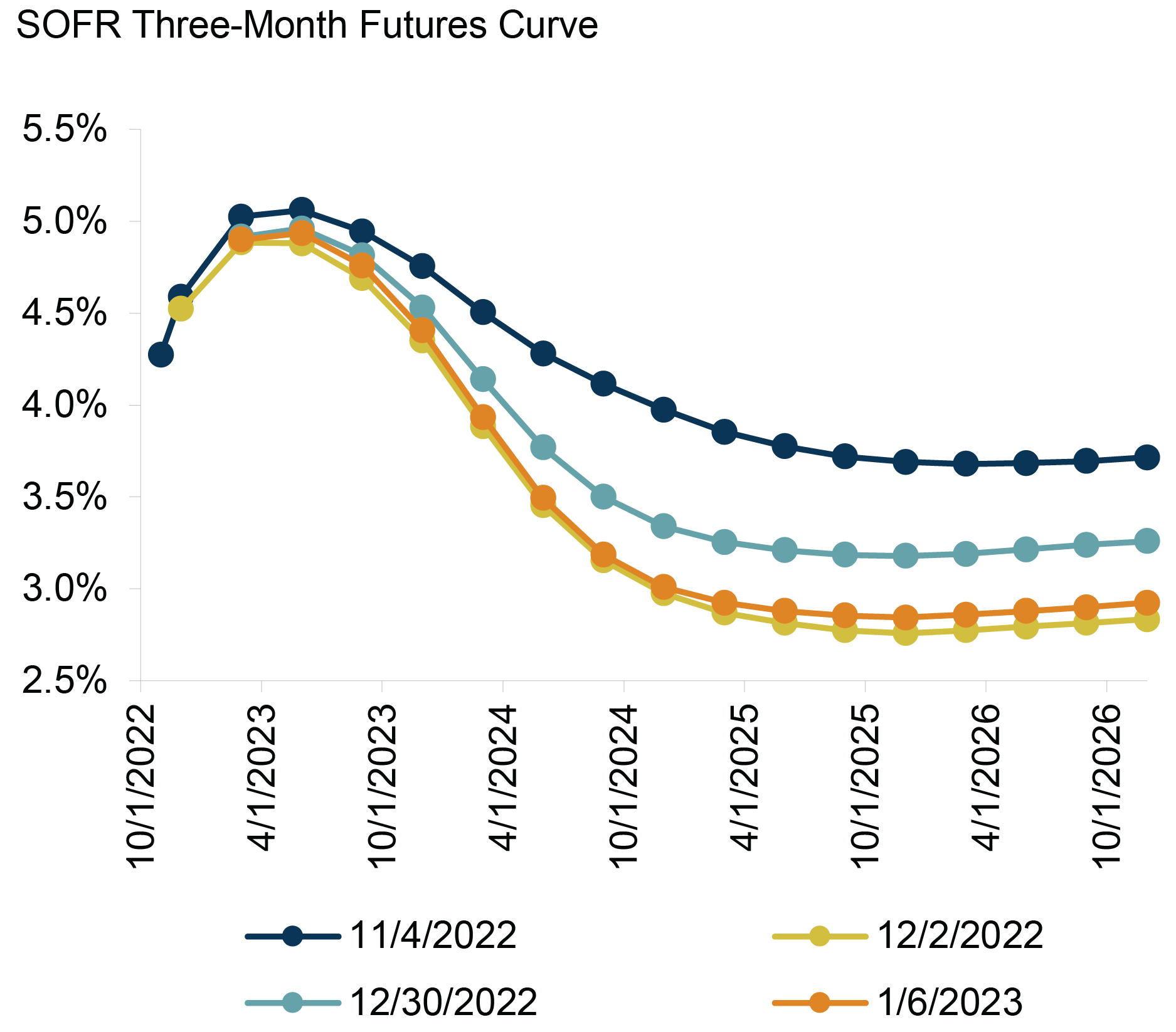

Investors’ views on inflation, recession risk, and monetary policy were fickle throughout much of 2022. However, in recent months, a positive bias has emerged, reflected in the downward shift in interest rate expectations and upward move in

securities prices since mid-October.1 Investors increasingly appear to be interpreting economic data as evidence that a dovish pivot is imminent – i.e., the Federal Reserve will soon stop hiking interest rates and be in a position

to cut them. As a result, bad news has become good news. Slowing job growth, dismal economic survey data, falling property values, negative real wage growth: It’s all good when viewed through the lens of inflation and monetary policy. While

investors briefly turned more pessimistic about the likelihood of monetary policy easing following Fed Chair Jay Powell’s hawkish statements in December, the positive bias won out. By early January, futures markets were pricing in interest

rate cuts of roughly 50 basis points in 2023 and almost 150 bps in 2024.2 (See Figure 1.)

Figure 1: Interest Rate Expectations Have Shifted Dramatically in Recent Months

Source: Bloomberg

But what has often been missing in this discussion of dovish pivots is the real economy and what may have to happen to it in order for this market narrative to play out. Because if investors get their wish and monetary policy changes dramatically

in the next 12 months, it will likely be because this bad news has gotten a whole lot worse.

Past the Peak?

The dovish pivot narrative has obviously been driven by the expectation that U.S. inflation – which has fallen for six consecutive months – will continue to decline at a fairly rapid rate.3 In fact, at year-end, markets were

anticipating that inflation would drop to 2.5% by the end of 2023. (See Figure 2.) On the one hand, it’s probably safe to assume that inflation has peaked for this cycle, given that (a) it has declined by 2.6 percentage points since June,

(b) supply chains are mostly debottlenecked, (c) wage growth is slowing, and (d) many commodity prices have fallen to levels present before Russia’s invasion of Ukraine.4 However, it’s also noteworthy that the Fed’s

success in slowing inflation thus far has occurred while China, the world’s second-largest economy, has been hampered by pandemic-related restrictions. While China’s full reopening will likely boost global economic growth, it could

also exert upward pressure on global inflation.

Figure 2: Inflation Is Expected to Decline Rapidly

Source: Bloomberg

History Lesson

But even if inflation continues to slow, does this automatically mean the Fed will respond by lowering interest rates? Futures markets indicate that investors think (a) the neutral interest rate remains between 2.5% and 3.0% and (b) the Fed will seek

to cut interest rates to this level even if there’s no pressing need to do so. But is this likely?

The history of the Fed suggests that it usually only shifts policy quickly in response to something bad, such as a credit crisis, economic downturn, severe market reaction, or, more recently, a global pandemic. The Fed is typically prone to keeping

policy either too tight or too loose for too long. And like many institutions, it can sometimes be guilty of “fighting the last war.” So excessive tightness/looseness in one period can result in an overcorrection in the next.

Next, consider what the Fed is actually saying. In December, Chair Powell stated that the central bank doesn’t plan to loosen monetary policy any time soon and will likely have to make it even more restrictive to ensure inflation is brought

under control. The Fed is likely concerned about prematurely claiming “mission accomplished” in part because the institution’s credibility has been damaged by the inflation spike in 2021-22 and the Fed’s claims that it

would be transitory. Moreover, Fed officials only have to look back at “the great inflation” of 1965 to 1982 to see what can happen when policy is loosened too quickly.

Finally, it’s important to remember that the market is part of the system that the Fed is attempting to control. The markets’ optimism, which may be keeping financial conditions looser than the Fed would like, could make it more likely

that the Fed keeps tightening policy. So, all things considered, the risk of over-tightening seems to be higher than the likelihood of a premature pivot.

The Rest of the Story

So what would cause the Fed to make a significant shift in policy? As we noted above, history suggests that it would most likely be a meaningful recession or market crisis – risks that certainly aren’t being reflected in today’s

earnings expectations or credit spreads. Investors appear to be focusing far more on what negative economic data means for interest rates than the potential implications for the real economy. When investors have reacted negatively to bad economic

news – like the weaker-than-anticipated December retail sales data released in mid-January – the response has been short-lived, as concerns about recession risk have quickly turned into optimism about that much-desired dovish pivot.

Consider what the market has welcomed as good news:

-

Wage growth is slowing. It’s understandable why investors and the Fed are happy with this development, given the impact that wages typically have on inflation. But it’s important to remember that the 4.1% increase

in average wages in 2022 – robust as that might sound – was still well below the 6.5% annual rate of inflation.5 And even if inflation continues to slow in 2023, the related slowdown in wage growth is likely to keep

consumers in the red for another year in real terms. -

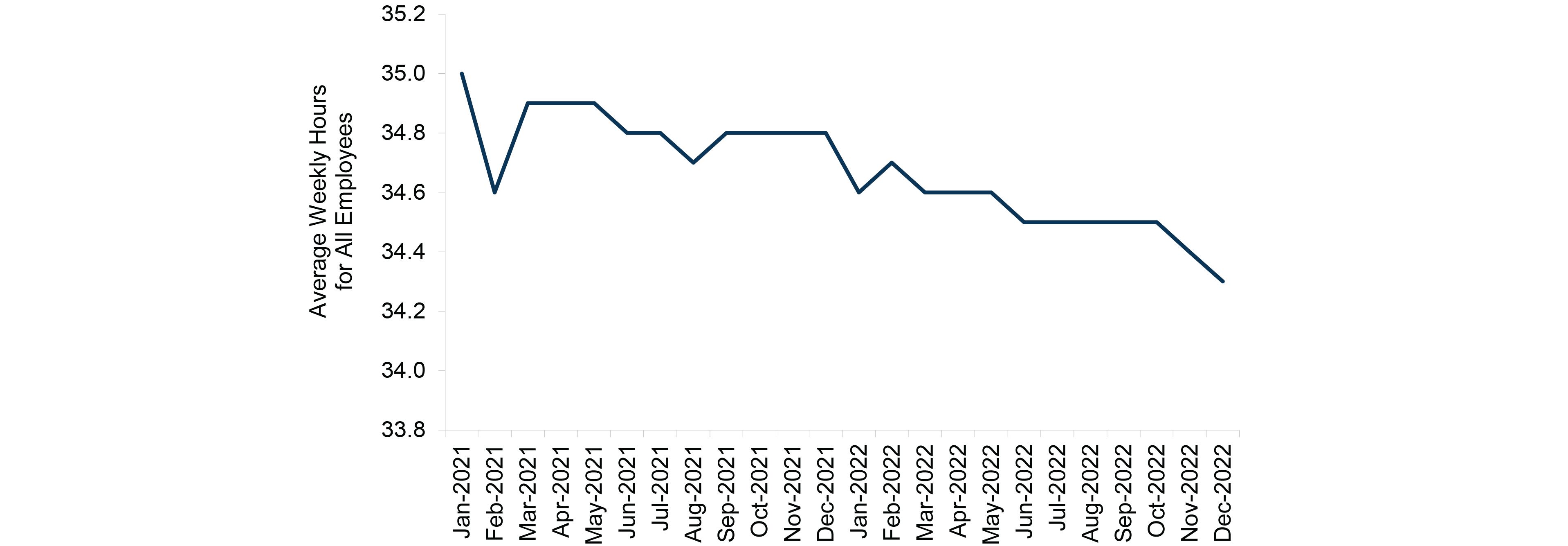

The job market is weakening. While the unemployment rate has been hovering near the 40-year low of 3.5% for several months and job gains remain above the pre-pandemic norm,6 a look beyond the headline numbers reveals

potentially negative trends. In December, average weekly hours per worker were down by 0.5 hours year-over-year, the equivalent of a loss of roughly two million jobs.7 (See Figure 3.) Moreover, the headline job gains might be

slightly misleading, as more people appear to be holding multiple jobs, as indicated by the discrepancy between the job increases recorded by the establishment survey and the household survey. (Double counting is less likely in the latter.)

These trends indicate that the labor market may be weaker than the low unemployment figure suggests.

Figure 3: Average Hours Worked in the U.S. Have Been Falling

Source: U.S. Bureau of Labor Statistics

-

Savings are declining. Trillions of dollars of fiscal and monetary stimulus helped support consumers, businesses, and asset prices in 2020 and provided fuel for the recovery in 2021. While the economy slowed in 2022, consumption

remained at fairly healthy levels for much of the year, partly because of the boost provided by the roughly $2.5 trillion in excess savings that households had accumulated during the prior two years.8 But the savings rate has

now plummeted below the pre-pandemic level, largely because consumers’ purchasing power has been eroded by negative wage gains. (See Figure 4.) That means consumers have had to spend down a chunk of this excess savings and therefore

may increasingly have to curb their spending.

Figure 4: The Personal Savings Rate Has Plummeted

Source: U.S. Bureau of Labor Statistics

-

Reliance on credit cards is growing. The drop in the savings rate and spike in the cost of living have unsurprisingly been accompanied by an increased reliance on credit cards. In November, consumers’ use of revolving

credit (primarily credit cards) rose by an annual rate of 16.9%. This wasn’t simply an anomaly caused by holiday spending, as this metric has risen by double-digit percentages in every quarter since 4Q2021.9 And this is

occurring at a time when credit has become more expensive: The average annual percentage rate (APR) on credit cards rose to 22.7% in December.10 -

Manufacturing and services activity appears to be slowing. The Institute for Supply Management’s surveys for both services and manufacturing indicated that activity contracted in December. Importantly, the former was

the first such contraction since May 2020, and the latter was the second consecutive monthly contraction and the lowest level since May 2020. While the Atlanta Fed currently estimates that the GDP growth rate in the fourth quarter will

be 3.5%, the near-term outlook for economic activity has clearly worsened.11

This is what is already occurring. In order for the Fed to shift gears meaningfully, these trends would likely have to get much worse. That would obviously

be bad news for corporate fundamentals and could potentially reveal economic damage caused by the pandemic that was temporarily masked by government largesse. We can’t predict what will happen in the next 12 months, but we think investors

who are waiting for an aggressive policy shift may discover that they should be careful what they wish for.

Credit Markets in 1Q2023: Key Insights

Where are Oaktree experts finding potential risks, opportunities, and relative value today? Going forward, Oaktree’s Performing Credit Quarterly will regularly highlight key insights that we believe investors should keep in mind when

navigating today’s markets.

(1) We are in a credit picker’s market

In 2022, interest rate risk was the major driver of relative performance in fixed income, as evidenced by the outperformance of floating- versus fixed-rate asset classes.12 But we think this situation may change if the U.S. and other major

economies slow. We believe that near-term default risk is low in most asset classes, as under 7% of outstanding bonds and loans are maturing before year-end.13 But we also think defaults are likely to increase from today’s ultra-low

levels. Moreover, we believe we could see significant volatility – and dispersion based on quality – in many fixed income markets if investors’ optimistic assumptions aren’t borne out.

(2) A void has grown in the funding market for large private equity deals

Banks were saddled with billions in hung bridge loans in 2022 after investor appetite for this debt collapsed. Banks are now seeking to reduce risk on their balance sheets and are therefore underwriting few new large-scale financings for leveraged

buyouts or mergers & acquisitions. Yet private equity sponsors are still seeking to complete deals, as they hold record-high amounts of dry powder. This has created attractive opportunities for those investors with the capital and flexibility

to fill this void, as the average yield spread offered for such financings is larger than what is found in traditional middle market deals.14 Moreover, lenders are now in a position to secure significant investor protections, a situation

that would have seemed impossible only one year ago.

(3) Fixed-rate bonds with long duration may offer attractive relative value

Investment grade and high yield bonds may become more attractive than loans in a weakening global economic environment, especially if investor concerns turn from interest rate risk to credit risk. In particular, we believe that bonds rated BB and

higher may be appealing to investors, given their minimal credit risk, attractive yields, and limited near-term maturities. Importantly, the effective duration of BB-rated bonds is 4.4 years, meaning many of these issuers have locked in low borrowing

costs for a significant period of time.15 However, the story is different for lower-quality issuers. The dramatic slowdown in high yield bond issuance in 2022 may signal trouble ahead for such borrowers, as they typically have shorter-duration

debt and thus could face rollover risk in the coming years.16

(4) “Junk loans” remain a significant concern

While leveraged loans outperformed high yield bonds in 2022, they may be more vulnerable moving forward, given rising borrowing costs, high leverage ratios, and, in many cases, eroding fundamentals. We’ve already seen a meaningful increase in

downgrades in recent months and a modest rise in defaults, albeit from a very low level.17 Looking forward, investors may face lower-than-anticipated recoveries when defaults do occur, due to the covenant-lite nature of most loans.

(Over 90% of loans issued in 2021 and early 2022 had minimal investor protections.18) As we noted last quarter, “the longer the fed funds rate remains significantly above the 10-year average, the more likely it is that the cracks in loan fundamentals that we’re seeing could widen and eventually

lead to greater instability and, potentially, a few collapses.”

(5) A potential sea change could create opportunities for bargain hunters

Many investors appear to believe that the macroeconomic conditions we’re seeing now, including a fed funds rate near 4.5%, are an aberration that will soon give way to a “normal” environment. That is, they think we’ll return

to the conditions present after the Global Financial Crisis when interest rates were near zero. But let’s remember that those conditions are not the norm historically. We’ll give Howard Marks the last word on what might be in store

for investors:

We’ve gone from the low-return world of 2009-21 to a full-return world, and it may become more so in the near term. Investors can now potentially get solid returns from credit instruments, meaning they no longer have to rely as heavily on riskier

investments to achieve their overall return targets. Lenders and bargain hunters face much better prospects in this changed environment than they did in 2009-21. And importantly, if you grant that the environment is and may continue to be very

different from what it was over the last 13 years – and most of the last 40 years – it should follow that the investment strategies that worked best over those periods may not be the ones that outperform in the years ahead. (Sea Change)

Oaktree’s Performing Credit Platform

Oaktree Capital Management is a leading global alternative investment management firm with expertise in credit strategies. Our Performing Credit platform encompasses a broad array of credit strategy groups that invest in public and private corporate

credit instruments across the liquidity spectrum. The Performing Credit platform, headed by Armen Panossian, has $60.21 billion in AUM and approximately 190 investment professionals.67

Endnotes

1 Securities prices refer to S&P 500 Index, ICE BofA US Corporate Index, and ICE BofA US High Yield Constrained Index, as of January 23, 2023.

2 Bloomberg.

3 U.S. Bureau of Labor Statistics for inflation data.

4 U.S. Bureau of Labor Statistics for inflation data.

5 U.S. Bureau of Labor Statistics.

6 U.S. Bureau of Labor Statistics.

7 The two million figure is based on the following Oaktree calculations: 0.5 hours * 52 weeks = 26 hours * 160 million workers = 4.1 million / 2080 hours (1 FTE hours / year) = 2 million.

8 Board of Governors of the Federal Reserve System.

9 Board of Governors of the Federal Reserve System.

10 The Balance, as of December 31, 2022.

11 Federal Reserve Bank of Atlanta, seasonally adjusted annualized rate, as of January 20, 2023.

12 Credit Suisse, JPMorgan, FTSE.

13 Calculations based on data from Bank of America and Credit Suisse, as of December 31, 2022.

14 From Oaktree observations in the market, as of January 23, 2023.

15 ICE BofA US High Yield Constrained Index, as of December 31, 2022.

16 ICE BofA US High Yield Constrained Index, as of December 31, 2022.

17 JP Morgan and Credit Suisse, as of December 31, 2022.

18 S&P Leveraged Commentary & Data.

19 The indices used in the graph are Bloomberg Government/Credit Index, Credit Suisse Leveraged Loan Index, Credit Suisse Western European Leveraged Loan Index (EUR hedged), FTSE High-Yield Cash-Pay Capped Index, ICE BofA Global Non-Financial HY European Issuers ex-Russia Index (EUR Hedged), Refinitiv Global Focus Convertible Index (USD Hedged), JP Morgan CEMBI Broad Diversified Index (Local), JP Morgan Corporate Broad CEMBI Diversified High Yield Index (Local), S&P 500 Total Return Index, and FTSE All-World Total Return Index (Local).

20 ICE BofA US High Yield Constrained Index.

21 JP Morgan.

22 ICE BofA US High Yield Constrained Index.

23 ICE BofA US High Yield Constrained Index.

24 ICE BofA US High Yield Constrained Index for all data in this bullet.

25 ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index (EUR hedged).

26 Credit Suisse.

27 ICE BofA Global Non-Financial High Yield European Issuer Excluding Russia Index.

28 ICE BofA US High Yield Index; ICE BofA Global Non-Financial High Yield European Issuer Excluding Russia Index.

29 JP Morgan.

30 ICE BofA US High Yield Constrained Index.

31 Credit Suisse Leveraged Loan Index.

32 JP Morgan.

33 JP Morgan.

34 Credit Suisse Western Europe Leveraged Loan Index (EUR hedged).

35 Credit Suisse.

36 JP Morgan.

37 JP Morgan.

38 JP Morgan.

39 JP Morgan CEMBI Broad Diversified High Yield Index. The Emerging markets debt section focuses on dollar-denominated debt issued by companies in emerging market countries.

40 BofA Global Research.

41 JP Morgan CEMBI Broad Diversified High Yield Index.

42 JP Morgan EM Default Monitor.

43 JP Morgan EM Default Monitor.

44 JP Morgan.

45 Refinitiv Global Focus Convertible Index.

46 Bank of America.

47 Bank of America for all issuance statistics in this bullet.

48 JP Morgan CLOIE BB Index.

49 JP Morgan CLOIE BBB Index.

50 JP Morgan.

51 JP Morgan.

52 JP Morgan.

53 JP Morgan CLOIE BBB Index, JP Morgan CLOIE BB Index.

54 Barclays CMBS 2.0 BBB Index.

55 Barclays.

56 JP Morgan.

57 Based on Oaktree observations in the market, as of December 31, 2022.

58 Deloitte Alternative Lender Deal Tracker, as of September 2022.

59 All statements in this bullet are based on Oaktree observations in the market, as of December 31, 2022.

60 Derived from Oaktree estimates, as of September 30, 2022.

61 ICE BofA US Corporate Index.

62 U.S. Department of the Treasury.

63 ICE BofA US Corporate Index.

64 ICE BofA Single-A U.S. Corporate Index.

65 ICE BofA Single-A U.S. Corporate Index.

66 ICE BofA US Corporate Index.

67 The AUM figure is as of September 30, 2022 and excludes Oaktree’s proportionate amount of DoubleLine Capital AUM resulting from its 20% minority interest therein. The total number of professionals includes the portfolio managers and research analysts across Oaktree’s performing credit strategies.

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial

instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including

broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent

of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree

providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation,

and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which

it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover,

independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2023 Oaktree Capital Management, L.P.

link

More Stories

The euro area bank lending survey

Economic Bulletin Issue 7, 2025

World Bank Group and Japan Housing Finance Announce MoU to Explore Joint Opportunities for Green Housing Finance