Published as part of the ECB Economic Bulletin, Issue 7/2021.

1 Introduction

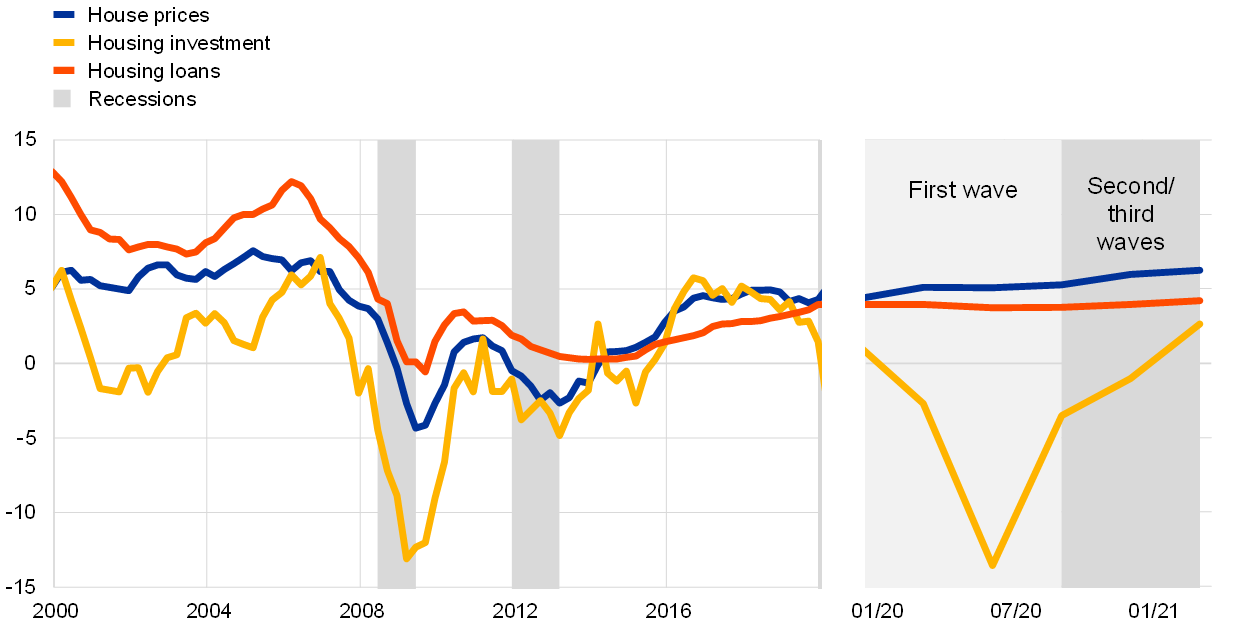

The euro area housing market was in a relatively long expansionary cycle before it entered the coronavirus (COVID-19) crisis.[1] On the eve of the COVID-19 crisis, the euro area housing market was on solid ground. In the last quarter of 2019, house prices, housing investment and housing loans were on an upward trend, supported by robust income developments and bank lending rates for house purchases at historical lows (Charts 1 and 2).[2] Given the phase in which the housing cycle stood, an economic shock like the COVID-19 crisis might have been expected to turn the cycle.

Chart 1

House prices, housing investment and housing loans in the euro area

(annual percentage changes)

Sources: Eurostat and ECB.

Note: Grey areas delimit recessions, as identified by the Centre for Economic Policy Research (CEPR) Euro Area Business Cycle Dating Committee.

However, the reaction of the euro area housing market to the COVID-19 crisis differed from that in previous crises owing to the different nature of the underlying shock.[3] The global financial crisis of 2008 originated in the US housing market and the sovereign debt crisis that started in 2010 stemmed primarily from financial shocks. Initially, the shock caused by the COVID-19 pandemic was unrelated to economic fundamentals and – especially in its early phases – afflicted the economy mainly through mandatory and voluntary restrictions on mobility aimed at containing the spread of the virus. These restrictions induced peculiar features compared with the global financial crisis and the sovereign debt crisis, notably as a result of their diverse impact on real and nominal housing dynamics and differing housing developments across countries. The particular nature of the COVID-19 pandemic triggered vigorous monetary, fiscal and macroprudential policy responses.

This article explores the developments in the euro area housing market during the pandemic and compares them with those in previous crises, paying particular attention to the role of policy support measures. Throughout, the article takes a holistic approach that covers developments in and prospects for euro area housing investment, house prices and loans for house purchase. Section 2 focuses on the diverse impacts on the euro area housing market of the first wave of the COVID-19 pandemic from the first to the third quarter of 2020, when strict containment measures had the greatest effect on activity. Section 3 elaborates on the subsequent resilience of the housing sector through the second and the third waves of the pandemic up to the second quarter of 2021, amid more targeted containment measures and significant policy support measures. Section 4 provides a forward-looking perspective on the prospects and risks for the euro area housing market.

2 The first wave of the COVID-19 pandemic – the diverse impacts of containment measures on the euro area housing market

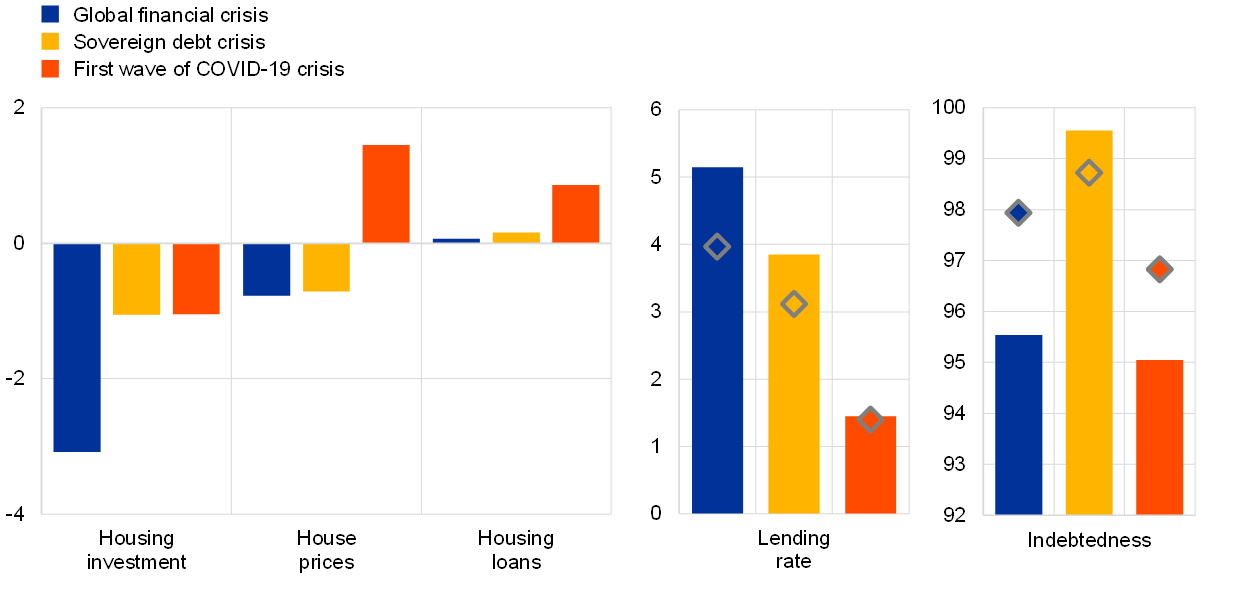

The containment measures in response to the first wave of the COVID-19 pandemic led to a divergence between real and nominal housing dynamics. The severe decline in mobility induced by containment measures and voluntary social distancing during the first wave of the pandemic had a negative impact on euro area housing investment, pushing it to 3.1% below its end-2019 level in the third quarter of 2020, broadly in line with the levels seen during the global financial crisis and the sovereign debt crisis (Chart 2). However, while in the previous crises deteriorating economic fundamentals hampered growth in house prices and housing loans, the COVID-19 shock did not weigh on the upward trajectory of prices and loans, which surpassed their levels in the fourth quarter of 2019 by 4.3% and 2.6% respectively in the third quarter of 2020, supported by resilient housing demand amid policy support measures (Box 1).[4]

Chart 2

Euro area housing market developments in the global financial crisis, sovereign debt crisis and the first wave of the COVID-19 crisis

(percentage changes; lending rate and indebtedness as percentages)

Sources: Eurostat, ECB and authors’ calculations.

Notes: Lending rate refers to the composite lending rate on housing loans. Indebtedness refers to the ratio of housing loans to annual gross disposable income. All variables are computed as average percentage changes over the reference periods, except the lending rate and indebtedness, where the bars refer to their levels in the quarter before the reference periods and the diamonds refer to the level in the final quarter of the reference periods. The reference periods are defined in Section 1.

The different nature of the COVID-19 pandemic compared with previous crises is also visible in the larger degree of diversity in housing investment dynamics across countries. Losses in housing investment during the first three quarters of 2020 varied widely, with nine countries recording gains and two countries (Spain and Malta) incurring larger losses than during the global financial crisis (Chart 3). These heterogeneous dynamics can partly be explained by the timing and relative degree of restrictiveness of containment measures,[5] with construction activity being temporarily halted in some countries.[6] Other factors included the initial fiscal support measures, which varied considerably across countries in terms of scale and timing,[7] as well as the different demographic structures of the national housing markets.

Chart 3

Housing investment across euro area countries during the global financial crisis and the first wave of the COVID-19 crisis

(average percentage changes)

Sources: Eurostat and authors’ calculations.

Note: In the legend, variable “x” refers to the average percentage change in housing investment during the respective reference periods in each panel, as defined in Section 1.

Demographic structures may also have induced diverse housing investment dynamics across countries, reflecting the differing impact of the first wave along the income distribution. Countries where a larger share of income is earned by poorer households experienced stronger declines in housing investment during the first wave of the pandemic.[8] Euro area survey data corroborates this, as lower-income households remained significantly less willing to purchase a house compared with pre-crisis levels by the end of the first wave of the pandemic in contrast to developments during the global financial crisis and the sovereign debt crisis (Chart 4). Instead, the intentions of medium and higher-income households to purchase property increased. This most likely resulted from these income groups’ high levels of accumulated savings induced by restrictions on the consumption of high-contact services.[9]

Chart 4

Households’ intentions to purchase property across income quartiles in the global financial crisis, the sovereign debt crisis and the first wave of the COVID-19 crisis

(average changes; net balances)

Sources: European Commission and authors’ calculations.

Note: The reference periods are defined in Section 1.

Box 1

The impact of restrictions on mobility on the housing market – a structural approach

This box examines empirically the impact of mandatory and voluntary restrictions on economic agents’ mobility following the outbreak of the coronavirus (COVID-19) pandemic on housing investment and house prices, accounting for several transmission mechanisms that are relevant for the housing market. On the basis of euro area aggregate data between the first quarter of 2000 and the first quarter of 2021, a Bayesian vector autoregression (BVAR) model exploits information from the dynamic interactions among seven endogenous variables: housing investment; real house prices; the composite lending rate on loans for house purchases; the stock of loans for house purchases; real GDP; consumer prices (HICP); and the shadow rate.[10] Following a large body of empirical literature,[11] the model identifies the main drivers of the housing market, imposing zero and sign restrictions on the co-movements among the endogenous variables upon the impact of various fundamental shocks.[12] To account for the specific characteristics of the COVID-19 crisis, the model includes – as an exogenous variable – a measure of the effective stringency of containment measures, namely the effective lockdown index. Conceptually, this index aims to isolate the economic impact of restrictions on mobility – accounting for both containment measures and voluntary social distancing – during the different waves of the pandemic.[13] In practice, the index acts as an augmented dummy variable, limiting the estimation problems induced by the abrupt and large fluctuations in economic developments observed since the start of the COVID-19 crisis.[14]

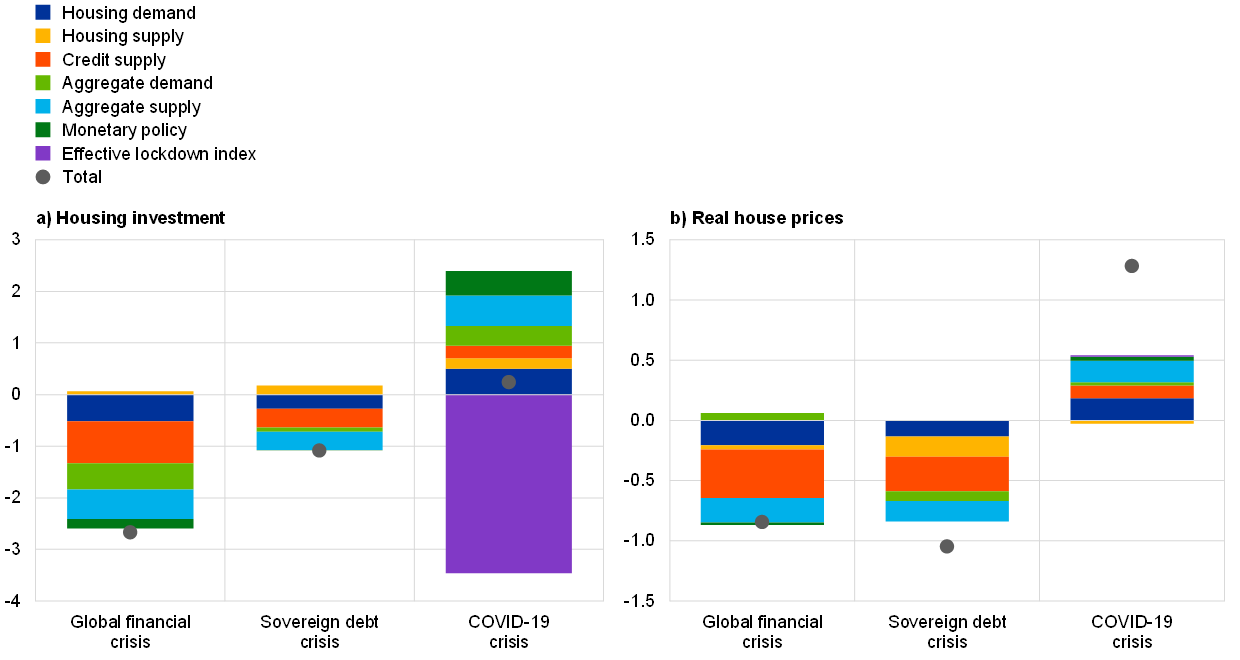

The historical decomposition of the drivers of housing investment and house prices highlights the peculiar effects of the COVID-19 crisis on the housing market (Chart A). During the global financial crisis and the sovereign debt crisis, economy-wide shocks and housing market-related forces, such as housing demand and supply, as well as credit supply shocks, were behind the protracted decline in both housing investment and house prices. In contrast to the two preceding crises, economic fundamentals mostly supported both housing investment and house prices, on average, over the COVID-19 crisis. However, containment measures induced a dichotomy between real and nominal housing dynamics. In fact, effective restrictions on mobility significantly weighed on activity, while they left house prices relatively unaffected throughout the COVID-19 crisis. Over the COVID-19 crisis, the identified shocks can explain housing investment relatively well, but less so for house prices. The gap between actual and explained house prices is the result of unidentified factors, such as risk aversion and possible changes in preferences, and a positive average growth rate.

Chart A

Drivers of housing investment and real house prices during the global financial crisis, the sovereign debt crisis and the COVID-19 crisis

(quarter-on-quarter percentage changes and percentage points)

Sources: Eurostat, Hale et al., op. cit., Lemke and Vladu, op. cit., Google residential mobility index, ECB, and authors’ calculations.

Notes: For comparability, the figures are reported as average quarter-on-quarter percentage changes and contributions over the reference periods, as defined in Section 1. The contribution of the constant term and other unidentified residuals (related for instance to risk aversion and possible changes in preferences) is not shown.

3 The second and the third waves – housing market resilience amid policy support measures

The housing market proved resilient during the second and third waves of the COVID-19 pandemic. In spite of the deterioration in the epidemiological situation that led to a tightening of restrictions in the fourth quarter of 2020, the euro area housing market gained further momentum. House prices remained on an upward trend, increasing in annual terms by around 6% in both the fourth quarter of 2020 and the first quarter of 2021, a pace not seen since mid-2007. Housing investment recovered further in the same reference period, settling close to its pre-crisis levels. These signs of significant resilience stemmed from both the supply side, as indicated by the momentum in value added and employment in construction and real estate, and the demand side, as suggested by the return of the number of transactions to pre-crisis levels in many euro area countries and the increased demand for mortgage loans. The milder impact of restrictions compared with the first wave and the significant stepping-up of fiscal and monetary policy measures, continuous favourable financing conditions, the increased attractiveness of housing for investment purposes – in view of forced savings – helped to strengthen housing investment and exert upward pressure on house prices.[15]

Fiscal policy measures were key in mitigating the negative effects of the second and the third waves of the pandemic on the housing market. These measures included short-time work schemes, targeted transfers to more vulnerable segments, cuts to personal income taxes, social contributions and indirect taxes. Policy interventions to support firms also contributed to mitigating the impact of the crisis on employment and income, and helped construction firms maintain housing supply.[16] These measures included direct support schemes for firms and the self-employed, partial compensation of losses, subsidies, tax deferrals and public guarantees on bank loans.[17] Other important policy tools were moratoria schemes, which provided households and firms with short-term relief through the suspension of principal and/or interest payments on loans, and very generous fiscal incentives for house renovation in some countries.

Monetary policy also provided key support to the euro area housing market by preserving favourable financing conditions for households and firms. First, the Pandemic Emergency Purchase Programme (PEPP) announced in March 2020, by impacting yields especially at the long end of the maturity spectrum, exerted significant downward pressure on lending rates. This was particularly pronounced for mortgage rates, as they are typically linked to longer-term interest rates. Second, the negative interest rate policy continued to contribute to historically low lending rates, thereby supporting bank lending. Third, the targeted longer-term refinancing operations (TLTRO III) offered attractive bank funding conditions, which banks passed on to firms and households, even for the non-targeted segment of the facility (i.e. housing loans).[18] Overall, according to the ECB bank lending survey (BLS), the ECB’s monetary policy measures contributed to an increase in housing lending volumes and an easing of bank lending conditions on new mortgages during the COVID-19 period.[19] As regards existing mortgages, households at the lower end of the income distribution seem to have benefited the most from the reduced interest rates via the so-called cash-flow effect of monetary policy, which increased their available resources for spending (Box 2).

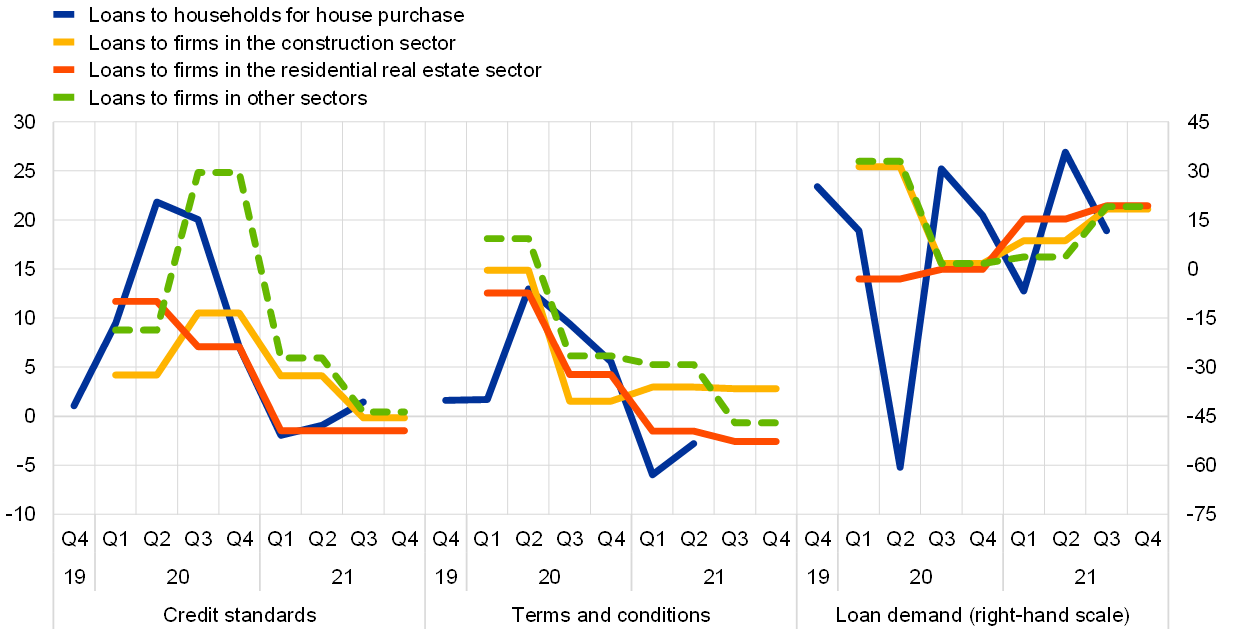

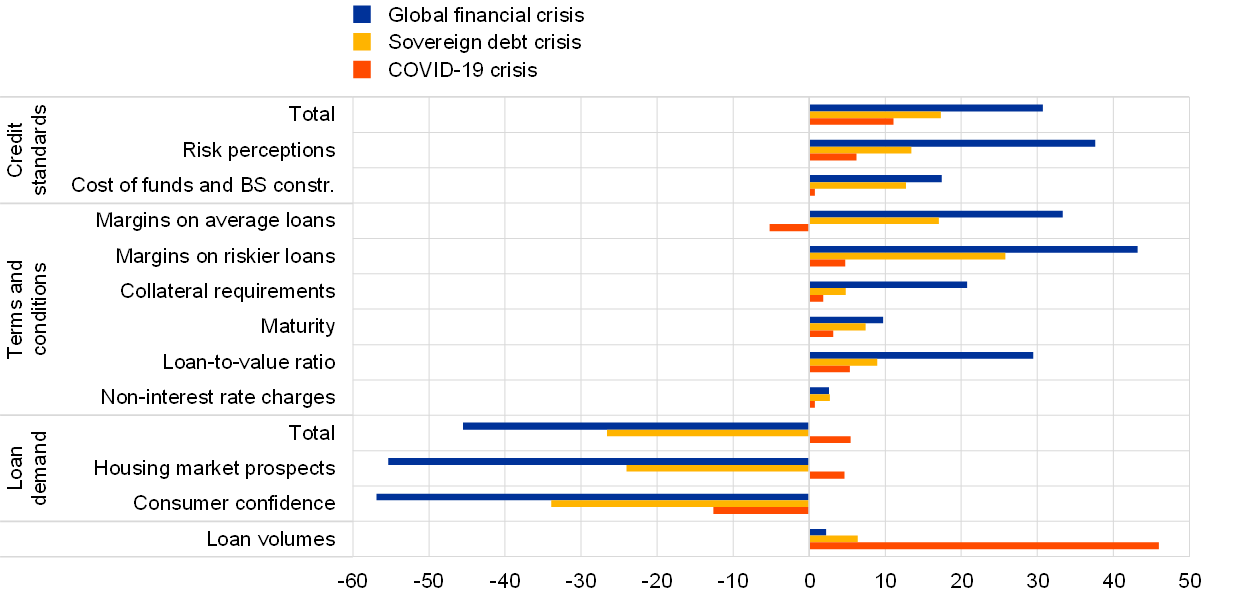

Financing conditions remained favourable, especially for less risky households, supporting the robust demand for housing. Apart from the first two months of 2020, flows of housing loans remained robust, with the annual growth rate of the loan stock reaching 4.2% in the first quarter of 2021, a rate not observed since 2008, significantly moving in tandem with house prices. Households’ demand for mortgages was met by historically low bank lending rates, which remained immune to the tightening in credit standards reported by banks in 2020 and to the increase in market rates in the first months of 2021. This muted response reflected favourable bank funding costs (buttressed by the policy support), but concealed a widening of lending margins for riskier borrowers and higher collateral requirements in the context of deteriorated perceptions of households’ creditworthiness. In the first half of 2021, tightening pressures on bank lending policies for housing loans vanished, primarily reflecting lower risk perceptions related to the improved economic outlook (Chart 5). The favourable developments observed during the second and third waves of the pandemic allowed households to experience a significantly smaller tightening of bank lending conditions during the COVID-19 period as a whole compared with previous crisis episodes (Chart 6).[20] The contribution of housing market prospects to loan demand was also strikingly different to that in previous crises in that it held up particularly well throughout the pandemic. Bank lending conditions for firms in the construction and the real estate sectors over the COVID-19 period were more favourable compared with those for firms in sectors that were hit harder by the containment measures.[21]

Chart 5

Bank lending conditions and loan demand for households and firms

(net percentages of banks)

Sources: ECB (BLS) and authors’ calculations.

Notes: The net percentages are defined as the difference between the sum of the percentages for “tightened/increased considerably” and “tightened/increased somewhat” and the sum of the percentages for “eased/decreased somewhat” and “eased/decreased considerably”. “Loans to firms in other sectors” is the unweighted average of loans to firms in manufacturing, services, wholesale and retail trade and commercial real estate. For loans to firms by sector, the questions have a biannual frequency, hence banks report on two quarters at once instead of one. Q3 21 and Q4 21 denote expectations indicated by banks in the July 2021 BLS.

Chart 6

Bank lending conditions for housing loans, loan demand and loan volumes

(for BLS indicators: net percentages of banks, quarterly average over crisis episodes; for loan volumes: flows in EUR billions, quarterly averages over crisis episodes)

Sources: ECB (BLS), ECB (BSI) and authors’ calculations.

Notes: The net percentages are defined as the difference between the sum of the percentages for “tightened/increased considerably” and “tightened/increased somewhat” and the sum of the percentages for “eased/decreased somewhat” and “eased/decreased considerably”. “Risk perceptions” is the unweighted average of “general economic situation and outlook” and “housing market prospects, including expected house price developments”. “Cost of funds and BS constr.” stands for “Cost of funds and balance sheet constraints”.

In a context of low interest rates, high uncertainty and large savings, housing demand has also been supported by investment motives. The demand for housing for investment purposes has been a distinctive feature of the recovery in housing markets that started in 2013.[22] This factor seems to have strengthened during the COVID-19 period, reflecting a further increase in the relative attractiveness of housing as an investment class and a further expansion of the availability of savings amid considerable economic uncertainty.[23] [24] Moreover, flows into real estate funds, albeit declining slightly in 2020, remained at relatively high levels, also as a share of residential investment. Although some of these funds could also be directed to commercial real estate or outside the euro area, this evidence suggests that private and institutional investors searching for yield and safety may have contributed to additional housing demand during the COVID-19 period.

Supply-side constraints have also exerted upward pressures on house prices. Constraints on housing supply have been an important factor behind housing market dynamics over the 2013-19 period. Following the significant decline in building permits in the aftermath of the pandemic outbreak, supply bottlenecks were further aggravated during the different waves of the pandemic (Chart 7). While in the first wave financing conditions and other factors (notably, containment measures) particularly constrained production, in the second and third waves supply bottlenecks were mainly due to labour and material shortages. The lack of (especially high-skilled) workers was also a major factor limiting production before the COVID-19 crisis,[25] but the shortage of materials reflected global supply-chain disruptions and a reallocation of resources induced by the outbreak of the pandemic, leading to increases in supplier delivery times and input costs. Overall, survey data suggest that, for construction firms, supply-side constraints increased relative to demand constraints during the COVID-19 period.

Box 2

Monetary policy and the cash-flow effect on households via mortgages

This box assesses the benefit households received from lower interest payments on their existing mortgage debt since the beginning of the ECB’s unconventional monetary policy in 2015. This so-called cash-flow effect of monetary policy contributed to the decrease in interest payments of the aggregate euro area household sector, which overall reached a record low of 2.2% of disposable income at the end of 2020 (Chart A, panel a). This positive effect helped households deal with the COVID-19 shock.

Chart A

Household interest payments and fixed rate mortgages

(panel a): percentages of gross disposable income; panel b): percentages)

Sources: Eurostat and ECB quarterly sectoral accounts (QSA) and ECB monthly data on euro area interest rates on loans and deposits (MIR).

Notes: Panel a): actual gross interest payments, i.e. including FISIM (financial intermediation services indirectly measured). Panel b): 12-month moving average of the share of new loans for house purchase with initial fixation period above ten years in total new loans for house purchase.

To investigate the distributional impact of this monetary policy transmission channel, we calculate the size of the advantage across the income distribution of households with a mortgage. Furthermore, we differentiate between the impact via adjustable rate mortgages (ARMs), which are relinked periodically to the change in short-term rates, and fixed rate mortgages (FRMs), which are affected by the change in long-term rates if households engage in refinancing their mortgage. Given the relatively large decrease in long-term rates since 2015 and the rising share of FRMs (Chart A, panel b), the advantage obtained via this channel is likely to have increased.

We calculate the benefit across the joint income distribution of households with a mortgage in the five largest euro area economies, combining household-level information on mortgages and income with country-level information on interest rates. Considering all households with a mortgage in 2014 (based on the second wave of the Household Finance and Consumption Survey (HFCS)), we calculate the income gain they booked at the end of 2020 compared with their initial situation in 2014 as a result of lower interest payments on their mortgages. For ARMs, calculations are based on developments in the short-term rate (EURIBOR 3-month), while for FRMs,[26] they take into account developments in long-term interest rates and refinancing volumes. In general, the latter increase with the size of the interest advantage, i.e. with the gap between long-term rates on new mortgages and the rate on outstanding ones.

Chart B

Income gain through lower interest payments on mortgages by income percentile

(percentages of household gross income)

Sources: ECB (HFCS, MIR) and authors’ calculations. Notes: The chart shows, for the households with a mortgage in 2014 in Germany, Spain, France, Italy and the Netherlands and grouped according to the aggregate income quintiles over those countries (x-axis), the average income gain booked at the end of 2020 compared with the initial situation in 2014 as a result of lower interest charges on adjustable (ARMs) and fixed rate mortgages (FRMs). For ARMs, this is calculated by the change in the short-term rate (EURIBOR 3-month) times the value of the outstanding ARMs in 2014. The gain due to lower interest rates on FRMs is calculated by the product of three components: the outstanding amount of FRMs in 2014, the average share of households that renegotiated their loans over the period 2015-20, and the average interest advantage they booked computed as the average difference between renegotiated rates and the rates on new mortgages five years earlier.

The cash-flow effect benefited all households with a mortgage and was on average around 0.9% of gross income via FRMs and 2% via ARMs (Chart B), supporting – all else being equal – household balance sheets, including during the COVID-19 period.[27] In the latter period, the income gain might have taken the form of extra savings, contributing to the resilience of the housing market.[28] Furthermore, the cash-flow effect benefited low income households in particular, which were most exposed to labour income losses during the COVID-19 period.[29] As such, lower interest payments might have mitigated the overall negative impact on the income of debtors, thereby also dampening inequality forces,[30] the likelihood of payment arrears and the need to make extensive and prolonged recourse to moratoria.[31] Finally, lower long-term rates encouraged both refinancing and a higher share of FRMs, so that households have been able to lock in the low interest rates, enhancing their debt sustainability and reducing their interest sensitivity in the event that monetary policy tightens.

4 Prospects and risks for the euro area housing market

Several factors are likely to support housing market prospects in the near term. The expected recovery in economic activity – sustained by a successful vaccination campaign in the euro area – should hold up households’ income and employment prospects, including when fiscal support gradually recedes. Financing conditions are likely to remain favourable, reflecting the policy support and the expected improvements in borrowers’ creditworthiness. Recent lending dynamics and indications from the BLS, which tend to display good leading properties in around two to three quarters in terms of house prices and housing investment, point to continued dynamism in the housing market in the coming quarters. Housing investment is likely to continue its positive trend observed since the third quarter of 2020, reinforced by resilient house prices relative to construction costs, improving real disposable incomes and buoyant intentions to buy and renovate properties (Chart 7). In addition, a part of the savings accumulated during the pandemic could be redirected into the housing market amid a low-yield environment and the increased relative attractiveness of housing for investment purposes. The share of residential property in real estate portfolios is likely to increase since it is perceived as a safer asset in times of uncertainty (housing is a primary need) entailing stable income streams (rents).

Nevertheless, the outlook for the housing market remains highly dependent on uncertainties related to the pandemic. Adverse developments related to the COVID-19 pandemic, such as the possible spread of new variants, might weigh on housing market prospects, and particularly on housing demand, as observed at the beginning of the pandemic. Amid high uncertainty, the withdrawal of policy support measures is an additional factor that could possibly limit prospects for the housing market if such policies were to be phased out before the recovery is on track. In addition, the overall increase in risk-free interest rates observed since the beginning of 2021 may exert upward pressure on mortgage rates. Moreover, the developments in shortages of raw materials and the associated increases in supplier delivery times and input costs could negatively affect construction activity and exert strong upward pressure on prices in the near term (Chart 7). This would contribute to keeping house prices in the euro area at an elevated level,[32] thus possibly increasing the importance of and need for macroprudential measures (Box 3).

Chart 7

Euro area supply constraints, construction input prices, supplier delivery times and intentions to buy and renovate

(input prices and supplier delivery times: deviation from baseline (50); intentions to buy and renovate: standardised levels; supply constraints: levels)

Sources: European Commission, IHS Markit and own calculations.

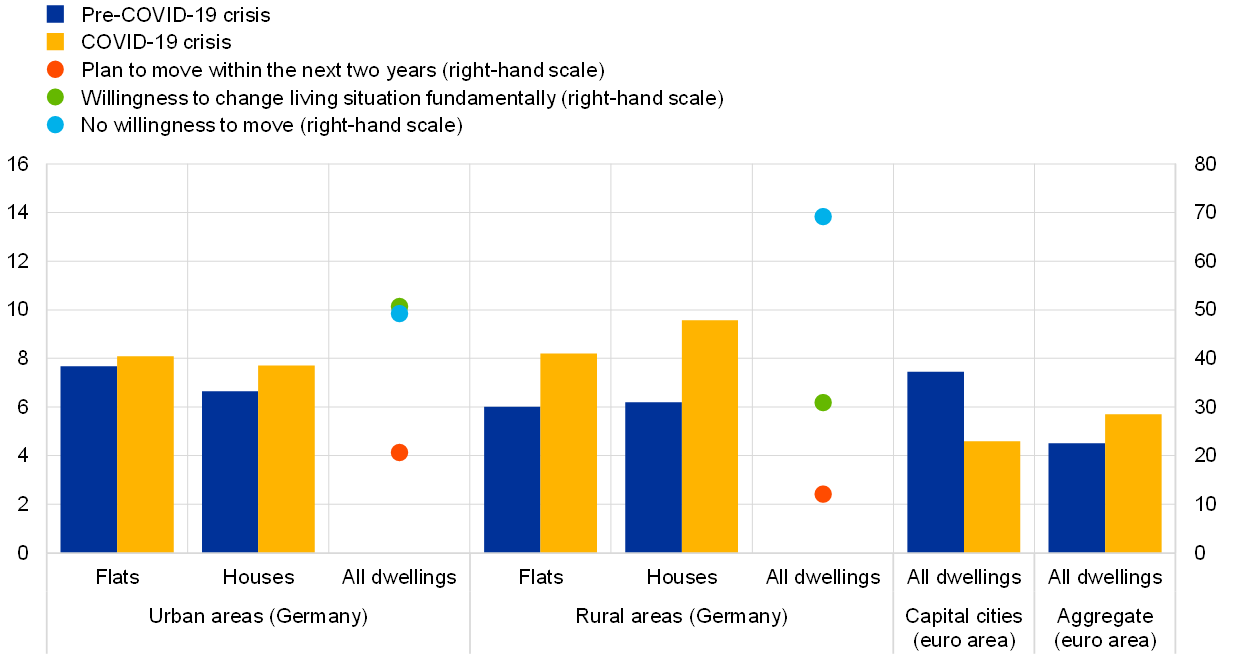

Changes in housing preferences may also affect the housing market going forward. The COVID-19 pandemic may bring changes in preferences and behaviour that could influence housing demand over the medium-to-long term. Should work-from-home arrangements become more prevalent, housing demand may partly shift away from city centres towards suburban and rural areas, as the opportunity costs associated with peripheral working places would decrease in tandem with commuting time.[33] This could contribute to limiting upward pressure on rent and house prices in large cities characterised by limited housing supply. As observed in other advanced economies,[34] preliminary evidence for some euro area countries tends to corroborate this narrative, hinting, for example, at buoyant house prices in rural areas in Germany and softening house price increases in capital cities in the euro area compared with the pre-pandemic period (Chart 8).[35] [36] The accelerated introduction of remote working arrangements slowed down the demand for commercial office and retail spaces, potentially opening up the possibility to convert some of these properties into residential housing in areas where supply is limited.[37] Both climate change and climate policies could also affect the housing market going forward. Investment in the energy efficiency of buildings could boost housing investment – also helped by fiscal incentives in some countries – thus lowering household spending on energy. In addition, properties meeting enhanced energy credentials could command higher prices, thus posing additional challenges for housing affordability.

Chart 8

Households’ plans to move and price developments in urban areas vis-à-vis rural areas

(average growth rates; percentages)

Sources: ECB, DESTATIS, ifo Institute, Eurostat, national sources and own calculations.

Notes: Residential property prices for urban areas in Germany are calculated as average growth rates of metropolis, cities not attached to a district and urban districts, and for rural areas, as average growth rates of densely and sparsely populated rural districts. The pre-COVID-19 period spans from the fourth quarter of 2016 to the fourth quarter of 2019, and the COVID-19 crisis period runs from the first quarter of 2020 to the first quarter of 2021. The “willingness to move” of households living in urban areas is calculated as the average of households’ responses from urban areas, suburban areas and small cities expressed as a percentage to a survey by the German ifo Institute. The “plan to move within the next two years” is calculated as the sum of percentages of households planning to move within the next six months, six to twelve months and within the next two years. The euro area aggregate series is a weighted average based on GDP weights, which includes Belgium, Germany, Estonia, Ireland, Spain, France, Italy, the Netherlands, Austria, Slovenia and Finland.

Box 3

Macroprudential policy for residential real estate before, during and after the COVID-19 pandemic

Prior to the COVID-19 pandemic, many euro area countries had activated macroprudential measures to address the build-up of residential real estate (RRE) vulnerabilities or to act as a prudent backstop. At the beginning of 2020, 14 euro area countries had in place borrower-based macroprudential measures (BBMs), such as loan-to-value (LTV), debt-service-to-income (DSTI), debt-to-income (DTI) or maturity limits.[38] In addition, seven euro area countries had activated macroprudential risk weight policies to increase the amount of capital banks need to hold against mortgage loans.[39] BBMs were put in place by many countries to act as a prudent backstop for lending standards, affecting only a small fraction of mortgage loan origination at the time of implementation, but providing an automatic limit to a potential widespread loosening of lending standards in the future. However, in some countries RRE vulnerabilities had been building up over preceding years, leading the European Systemic Risk Board (ESRB) to issue warnings and recommendations to six euro area countries in September 2019.[40] In some countries, macroprudential measures were therefore put in place to more actively contain the build-up of RRE vulnerabilities and increase bank resilience against associated systemic risks.

Following the outbreak of the pandemic, in line with the countercyclical nature of macroprudential policy, some national authorities eased macroprudential measures for RRE in order to limit the possible amplification effects of a tight macroprudential stance. In Malta, Portugal, Slovenia and Finland, national authorities adjusted existing BBMs at the height of the pandemic in spring 2020, fearing that the pandemic shock could constrain market access for solvent borrowers facing temporary income and liquidity shocks.[41] Two countries provided some capital headroom to absorb losses and meet credit demand. In the Netherlands, the planned implementation of an LTV-dependent risk weight floor for mortgage loans was postponed, and, in Finland, the existing risk weight floor for IRB mortgage loans was not extended beyond 2020. All of the above measures provided relief to new borrowers and banks alike and complemented other support measures, such as loan repayment moratoria or short-term working schemes (Section 3).

In most euro area countries, authorities did not adjust the BBMs that were already in place, as they were considered to be prudent back-stops for which adjustment had not been foreseen throughout the cycle. In addition, depending on the legal basis, there was a possibility that adjusting BBMs might involve lengthy processes compared with capital measures. However, Belgium and Estonia extended the application of risk weight measures on mortgages (under Article 458 of the CRR) in 2021 to retain bank resilience for accumulated RRE risks. Since existing risk weight measures affect minimum requirements or sectoral buffers, they might need to be released in the event that risks and losses in the RRE market materialise.

Chart A

Macroprudential measures should be considered in countries where vulnerabilities continue to build up as short-term downside risks recede

a) Annual RRE price growth in the fourth quarter of 2019 and the first quarter of 2021

(panel a): percentages; panel b): current policy considerations for RRE macroprudential measures)

b) Current policy considerations for RRE macroprudential measures

Sources: ECB and authors’ calculations.

Notes: Panel a): Hollow dots refer to the values in the fourth quarter of 2019; coloured dots refer to the values in the first quarter of 2021 (the fourth quarter of 2020 for Cyprus and Finland). Average overvaluation denotes the average of the price-to-income ratio and the results of an econometric model in the fourth quarter of 2019.

Going forward, as pandemic risks recede, further macroprudential measures for RRE should be considered in countries where RRE vulnerabilities continue to build up. Robust house price and mortgage loan growth continued throughout the pandemic, particularly in countries with pre-existing RRE vulnerabilities (Chart A, panel a). Nevertheless, the divergence between the RRE and economic cycles during the COVID-19 pandemic can imply downside risks in adverse growth scenarios, especially if government support is scaled back too early. In this context, macroprudential measures should be used in countries where vulnerabilities continue to build up as short-term downside risks recede (Chart A, panel b). In this regard, Luxembourg activated BBMs at the end of 2020, while in spring 2021 the Netherlands confirmed its intention to activate the LTV-dependent risk weight floor for mortgage loans.[42] These actions notwithstanding, further macroprudential measures could be needed in some euro area countries if current trends in RRE markets continue.

5 Conclusion

This article discussed developments in the euro area housing market since the outbreak of the COVID-19 pandemic. The mandatory and voluntary restrictions on economic agents’ mobility in response to the first wave of the COVID-19 pandemic had a strong impact on activity without significantly impairing the upward trend in prices and loans, in contrast to the global financial crisis and the sovereign debt crisis. Moreover, the first wave of the pandemic induced greater diversity in housing investment across countries compared with previous crises, which is partly explained by the varying impact of restrictions along the income distribution.

Several factors supported the housing sector throughout the pandemic. The resilience of the housing market originated in part from the declining impact of restrictions after the first wave. Other factors included fiscal, monetary and macroprudential policy measures, continuously favourable financing conditions, the increased attractiveness of housing for investment purposes, as well as supply-side bottlenecks exerting upward pressure on house prices without significantly weighing on activity.

Overall, pandemic-related uncertainties and associated structural changes will continue to influence the prospects for the housing market. The broad-based economic recovery and the use of the large stock of accumulated savings are likely to support housing market prospects going forward. However, the outlook remains uncertain and depends on how the pandemic develops and the timing of the withdrawal of policy support. Changes in housing preferences may also lead to a reallocation within the housing market, away from commercial and urban residential properties and towards suburban and rural residential real estate. Heterogeneous developments across households are likely to persist and possibly intensify.

link

More Stories

The euro area bank lending survey

Economic Bulletin Issue 7, 2025

World Bank Group and Japan Housing Finance Announce MoU to Explore Joint Opportunities for Green Housing Finance